Scooter’s Coffee®

What Is Scooter’s Coffee?

Scooter’s Coffee is a quick-service coffee franchise offering espresso-based drinks, smoothies, baked goods, and related food items. Stores primarily generate sales from drinks and associated food products and operate through drive-thru windows, indoor ordering/dine-in and service-counter formats. Franchise locations are typically configured as drive-thru kiosks in parking lots, strip-center end-cap spaces, free-standing buildings, or inside institutional sites such as hospitals, malls, schools, airports, and sporting venues.

Scooter’s Coffee Franchise: Pros and Cons

The franchise's biggest strength is its scale-906 total outlets with 882 franchised units (both top 10% for Food & Beverage), which delivers brand recognition and supplier leverage; its biggest risk is elevated turnover, with 24 reacquired outlets (top 5%), indicating franchisees are exiting at higher-than-normal rates.

Pros

Cons

Lawsuits & Legal Risk

Scooter’s Coffee: Part 1 - Active enforcement of system standards: recent AAA collection actions allege unpaid royalties, marketing contributions, technology fees, and supply‑chain charges by franchisees. Part 2 - Advice: review royalty and marketing fee calculations, supply agreements, cure/termination clauses, audit/accounting rights, and arbitration provisions in the FDD and franchise agreement.

Territory Protection

Scooter’s Coffee grants site-specific, non-exclusive territory rights via Franchise and MSD Agreements, providing Franchised Locations or Development Areas rather than exclusive territories. They are contingent on meeting development schedules and performance quotas; the franchisor may develop nearby units, affecting market density, and sell via e-commerce and other alternative distribution channels.

Training & Support

Scooter’s Coffee provides a Comprehensive 142-hour training curriculum designed to prepare four individuals for launch, combining classroom instruction, systems training, and hands-on operational practice. The program includes on-site launch assistance for operational readiness, with on-site support available post-launch and additional support services subject to separate fees; travel and lodging expenses are the responsibility of the franchisee.

Franchisee Stability

Scooter’s Coffee earns a Good Stability Score. Three-year turnover of 2.79% is well below the typical Food & Beverage franchise (around 6%). Out of 58 total exits, ceased operations dominated with 46, alongside 8 franchisor buybacks, 3 terminations, and 1 non-renewal.

The dominance of ceased operations points to location-level economics: operators likely chose to close underperforming locations rather than systemic franchisor-franchisee friction. Beyond its industry-relative position, a 2.79% three-year turnover rate is genuinely exceptional in absolute terms across all of franchising. Ask the franchisor for detail on where and why closures clustered, and verify unit-level recovery plans and historical sales at affected sites. For prospective franchisees, examine unit-level economics in the geographies where closures have concentrated.

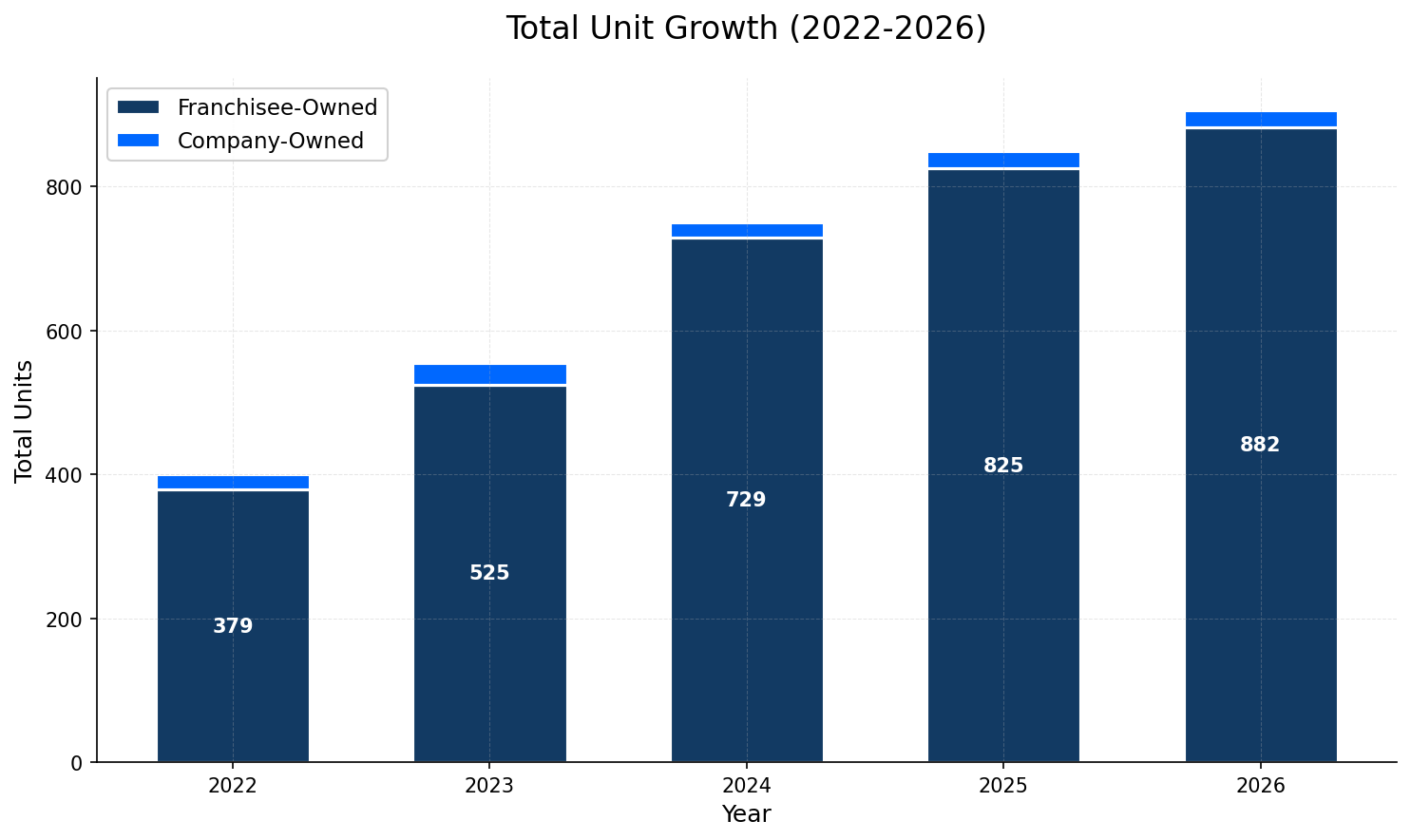

Unit Growth Analysis

Scooter’s Coffee has grown from roughly 400 to 906 units since 2022 but is now slowing to about 6.7% year-over-year, signaling a move from rapid roll-out toward market saturation. For a new owner that means you’re buying into an established, mostly franchised system where the upside is steady unit cash flow rather than big territory appreciation - expect tougher competition for prime sites, more emphasis on squeezing margin from existing locations, and the need to validate unit-level economics carefully before committing.

Frequently Asked Questions

Is Scooter’s Coffee a good franchise to own?

Whether Scooter’s Coffee is a good franchise depends on your goals, experience, and local market. Key factors from the 2026 FDD: Scooter’s Coffee operates 906 locations, received a legal risk score of 93/100, a training and support score of 100/100. Financial performance data is disclosed in Item 19. Prospective franchisees should review the full Franchise Disclosure Document and consult with a franchise attorney before making any investment decision.

What is the failure rate of Scooter’s Coffee franchises?

In the 2026 FDD, Scooter’s Coffee reported 1 terminated franchises and 1 non-renewals out of 906 total locations. Franchise closures can result from many factors including market conditions, operator decisions, lease expirations, and franchisor enforcement actions. The FDD's Item 20 provides the most detailed unit turnover data.

How long does it take to break even with a Scooter’s Coffee franchise?

Break-even timelines for Scooter’s Coffee franchises are not disclosed in the 2026 Franchise Disclosure Document. Break-even periods vary significantly based on initial investment level, local market conditions, operating costs, and revenue ramp-up speed. Prospective franchisees should build a pro forma financial model using Item 7 cost estimates and, where available, Item 19 financial performance data from the FDD.

Is Scooter’s Coffee a franchise or a corporate-owned business?

As of the 2026 FDD, Scooter’s Coffee operates 882 franchised locations and 24 company-owned locations. Franchise opportunities are available through the franchisor's disclosure process.

Interested in Scooter’s Coffee?

Get more information and connect with the franchise directly.