Family Financial Centers®

What Is Family Financial Centers?

Family Financial Centers is a franchise for operating financial services centers that provide check cashing, money orders, wire transfers, electronic bill payment, tax preparation, bookkeeping and other financial products offered through third‑party vendors. Franchisees operate primarily from brick-and-mortar locations - either stand-alone centers typically in strip shopping centers or malls (about 800–2,000 sq ft) or a scaled "Store 'N Store" model located inside another retail business. The primary target customers are the general public (individual consumers/B2C).

Family Financial Centers Franchise: Pros and Cons

The franchise's most notable strength is its low $10,125 initial franchise fee (bottom 10%), leaving more cash for build-out and early operations. The biggest risk is the manager equity requirement of 50% (top 5%), which forces large manager investments and can complicate recruiting and deal making.

Pros

Cons

Lawsuits & Legal Risk

Family Financial Centers reported no material legal proceedings,

Territory Protection

Family Financial Centers grants a non-exclusive protected area (roughly 0.1–1 mile in metros; up to 2.5 miles in smaller/rural markets); the franchisor will not establish another Financial Center there but may acquire and rebrand MSBs, and protection is not contingent on performance. No right of first refusal; relocations require approval.

Training & Support

Family Financial Centers provides a robust 77-hour training curriculum designed to prepare two staff members for launch through a structured instructional program. The program includes on-site launch support for operational readiness; travel and lodging expenses are the responsibility of the franchisee, and on-site assistance is available for an additional fee.

Franchisee Stability

Family Financial Centers earns a Good Stability Score. Three-year turnover of 5.45% sits below the typical Business Services franchise (around 7%), and it is modest compared with industry peers. Out of 9 total exits, ceased operations dominated with 9, alongside no terminations, no non-renewals, and no franchisor buybacks.

The dominance of ceased operations suggests location-level economics: operators chose to close underperforming locations, not franchisor-franchisee friction. That pattern can arise from local market softness, difficult site economics, or owner-level decisions leading to closures rather than franchisor-initiated exits. About 55 franchised outlets in the most recent year provide a moderate system size to judge these closures against. For prospective franchisees, examine unit-level economics in the geographies where closures have concentrated, and speak with nearby current and former owners about local demand and cost structure.

How Much Does It Cost to Open a Family Financial Centers Franchise?

Opening a Family Financial Centers franchise requires a total initial investment of $224,470 to $308,670, according to the 2025 Franchise Disclosure Document. This range covers the franchise fee, real estate, equipment, training, and initial working capital needed to launch and operate through the early months.

Minimum Investment

Maximum Investment

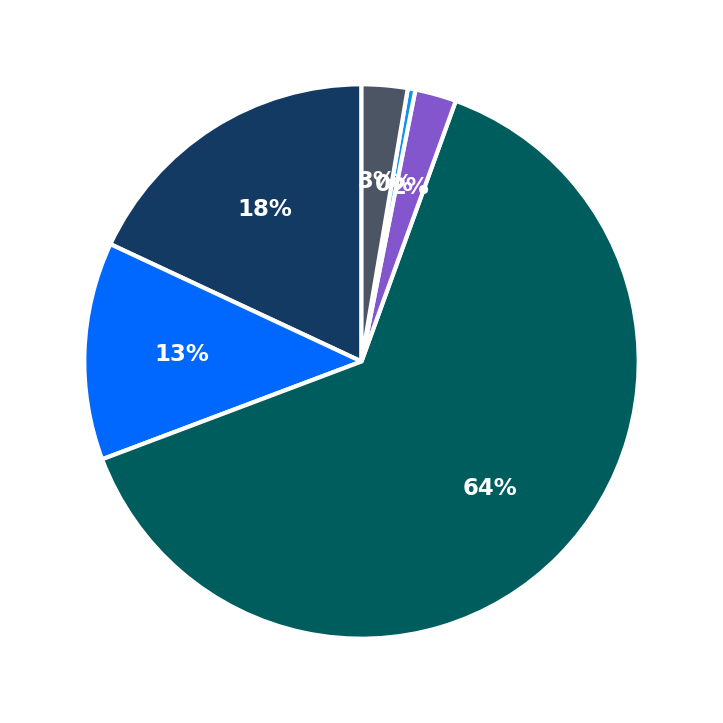

Minimum Investment Breakdown

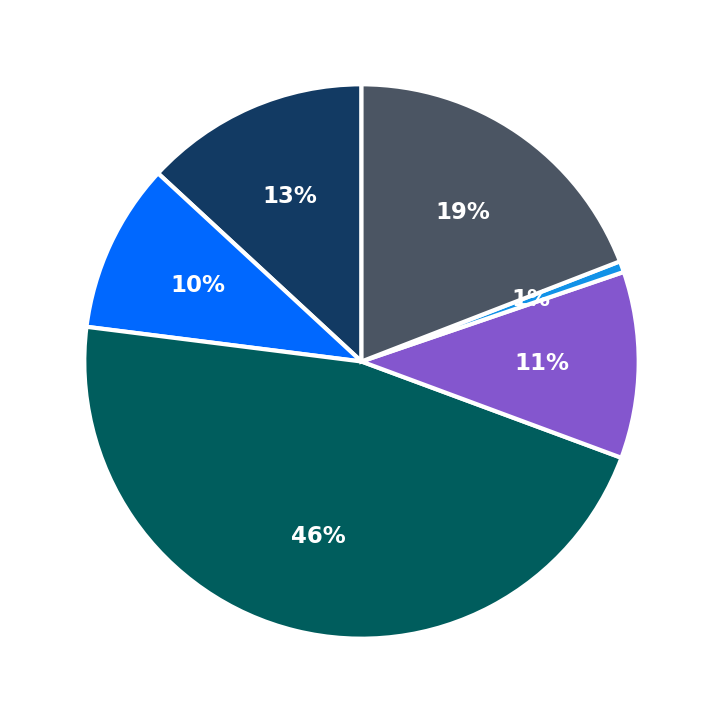

Maximum Investment Breakdown

Investment Analysis

This investment analysis is coming soon. Have ideas for other analyses you'd like us to add? Get in touch.

The initial investment amounts shown are estimates only. Actual costs may vary based on location size, business model, and multi-unit ownership arrangements. We recommend reviewing the full Franchise Disclosure Document for complete details.

Frequently Asked Questions

Is Family Financial Centers a good franchise to own?

Whether Family Financial Centers is a good franchise depends on your goals, experience, and local market. Key factors from the 2025 FDD: Family Financial Centers operates 52 locations, received a legal risk score of 100/100, a training and support score of 84/100. Financial performance data from Item 19 is being compiled. Prospective franchisees should review the full Franchise Disclosure Document and consult with a franchise attorney before making any investment decision.

Is a Family Financial Centers franchise worth the investment?

The value of a Family Financial Centers franchise investment depends on factors such as location, operator experience, and market demand. The initial investment ranges from $224,470 to $308,670. Franchise investments carry inherent risk, and prospective buyers should conduct thorough due diligence before committing capital.

How long does it take to break even with a Family Financial Centers franchise?

Break-even timelines for Family Financial Centers franchises are not disclosed in the 2025 Franchise Disclosure Document. Break-even periods vary significantly based on initial investment level, local market conditions, operating costs, and revenue ramp-up speed. Prospective franchisees should build a pro forma financial model using Item 7 cost estimates and, where available, Item 19 financial performance data from the FDD.

Is Family Financial Centers a franchise or a corporate-owned business?

As of the 2025 FDD, Family Financial Centers operates 52 franchised locations and 0 company-owned locations. Franchise opportunities are available through the franchisor's disclosure process.

Interested in Family Financial Centers?

Get more information and connect with the franchise directly.